Embracing the Death of DB: Alternatives Manager Capital Raising in the UK Moving Forward?

The mansion house reforms triggered a strategic shift in pension fund allocation that could potentially unlock £75 billion in capital for private markets funds in the UK, leading to a 12% boost in the average earner’s pension savings.

The rise of DC assets going into private markets presents an opportunity for GPs to raise significant capital from this new channel.

Wealth distribution is also noteworthy, holding half of all global assets, while representing less than 5% of alternative investment strategies (Bain & Co, 2022).

This paper details the future of the UK investor landscape and guides GPs on how to establish a lasting foothold.

It covers the necessary product structures and sales team efforts as well as examples of firms that have managed to get ahead of the curve and consolidate themselves as market leaders.

Movement in UK Pension Money

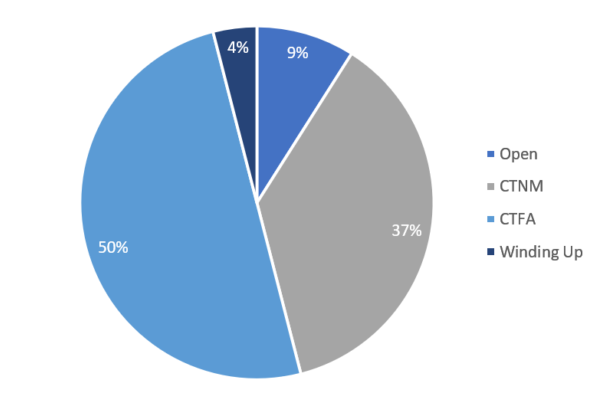

DB pension assets in the UK have been dwindling at a rapid pace, experiencing a closure rate of 26% over the last decade, with only 9% of schemes remaining open and half of them no longer accruing future years. Active membership has also decreased by 65% over the last decade.

Figure 1: Distribution of DB schemes by status in 2022

Source: The Pensions Regulator: https://www.thepensionsregulator.gov.uk/-/media/thepensionsregulator/images/db-landscape-2022/figure-1-distribution-of-schemes-by-status.ashx

- Open – schemes where new members can join the DB section and accrue benefits.

- Closed to new members (CTNM) – existing members continue to accrue benefits.

- Closed to future accruals (CTFA) – Existing members cannot accrue new years of service.

- Winding up – schemes that are in the process of winding up.

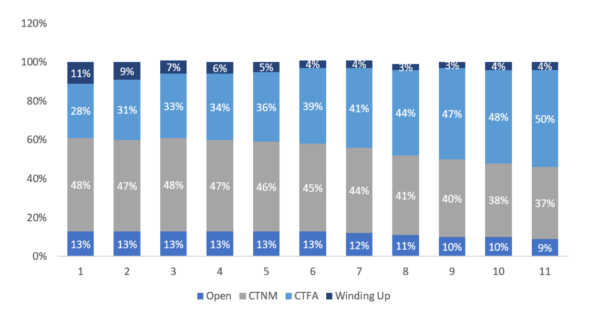

Figure 2: Distribution of DB schemes by status and year

Source: The Pensions Regulator: https://www.thepensionsregulator.gov.uk/-/media/thepensionsregulator/images/db-landscape-2022/figure-2-distribution-of-schemes-by-status-and-year.ashx

Insurer buyouts of DB pensions is also causing the decline. In a buyout the pension plan transfers investment and macroeconomic risk to the acquiring insurer, where the insurer is now required to meet the needs of scheme members. This has had repercussions for private markets, with DB pensions lowering their allocations, reluctant to tie up capital. They have even gone as far as selling their private assets on the secondary market to expedite the buyout process.

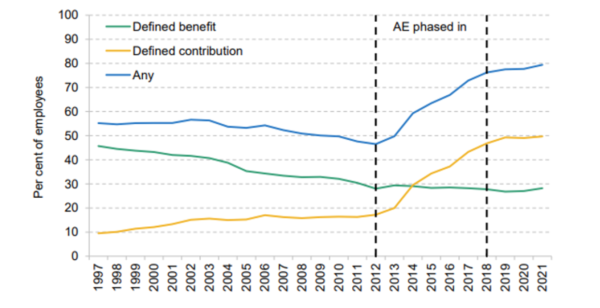

Auto enrolment (AE) was gradually phased in from 2012 and the percentage in pension participation grew massively, entirely within DC schemes. In 2021, half of all workers were contributing into their DC pension plan. Most of these individuals are the younger generation, so we are seeing many more pension pots, however the majority are very small. This trend will continue to occur, and we will see almost all private pension money in 30 years be within DC pension plans. The effect of AE can be seen in Figure 3.

Figure 3:

Source: Institute for Fiscal Studies, 2023: How important are defined contribution pensions for financing retirement?

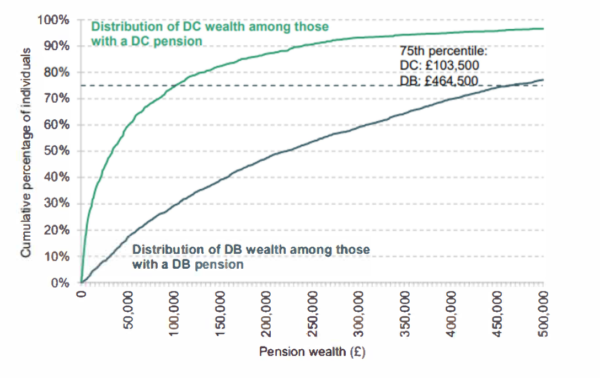

For individuals aged 50 to 59, nearing retirement, the median value of DC pension accounts was £33,500, compared to £220,500 for DB accounts. Factors contributing to this gap include longer tenure for DB plans, higher contribution from both employees and employers and market returns impact DC pensions, while having minimal effect on DB plans.

Figure 4 below illustrates the wealth distribution associated with DB and DC plans. While there is a significant difference in the distributions, this is partially due to the current average longer tenure for DB schemes. As time goes on the distribution will tighten and wealth in DC will increase. Therefore, in the long term, DC assets will become a valuable source of capital for private markets GPs.

Figure 4: Distribution of Total DC wealth and Total DB Wealth among 50-59 Year Olds

Source: Graph using the numbers from the Wealth & Assets Survey, Round 7 (2018-20)

Biggest UK Capital Raising Opportunities Moving Forward and What GPs Need to Target Them:

DC Pension Schemes: Progression in DC regulation for private markets

Projections indicate that DC assets are poised to double to £1 trillion by 2030 (ABI, 2023). In parallel the largest schemes are increasing allocations into private markets. NEST invested 15% of their 2023 allocation into illiquid assets, while Scottish Widows are committed to bringing their illiquid assets allocation to 15-20%.

Historically, illiquidity, cost, and allocation constraints limited DC investments into private markets but over the past year, new regulation and incentives are solving many of these challenges.

DC pension schemes must adhere to funds with daily pricing, daily transactions, and highly standardised subscription and redemption procedures. Additionally, there’s a strict 75-basis point charge cap on DC default funds. These requirements are not aligned to the illiquid nature and high fee of private market funds. However, in April 2023, the inclusion of performance fees within the 75 bps charge cap for DC funds was removed. Shortly thereafter, the Mansion House reforms were introduced, imposing schemes to invest 5% of their total allocation into UK private markets thus guaranteeing a growing DC commitment to the space.

The next change that schemes are now lobbying for is more flexibility on how they can invest. As Scottish Widows has highlighted, given their approx. 15-20% allocation into global private markets, the 5% UK private markets allocation requirement is an enormous new tax roughly 33% of their allocation will be invested within the UK, creating a geographical limitation. (Andrew Warwick-Thompson, 2023)

Moreover, the DC market currently operates under a prevailing culture that prioritises cost as the primary factor. The consequence is a race to offer the most competitive prices. This approach comes at the expense of investment performance and a comprehensive focus on achieving such performance.

However, consolidation will likely counteract this “cost is king” culture. The DC master trust market has decreased from 89 schemes before authorisation to 36, with further reductions expected. This consolidation process enables the attainment of greater scale, which, in turn, enhances the capacity to provide better outcomes for the scheme’s members. Government authorities are urging small schemes (with <£100 million) to assess whether they are delivering value for money. If not, consolidation is being recommended as a course of action. DC consolidation has the potential to increase leniency on fees and elevate the calibre of decision-makers at the helm, improving the long term outcome of DC investment in private assets.

While some limitations remain, the DC market is growing rapidly and over the last year has seen major developments that will lead to significantly more DC assets going into private markets. This creates an opportunity for GPs to get ahead and invest in a lasting strategy to capture substantial market share in the space.

DC Pension Schemes: Creation of DC Private Markets Evergreen Funds

For DCs to access DC assets they need to create a fund that adheres to the daily pricing, daily transactions, and standardised subscription and redemption procedures.

In 2016, Partners’ Group (PG) released the Generations Fund for UK DC schemes and became the first GP to target the space. Funds’ AUM currently sits at £700m and gives investors access to Partners’ Group’s full range of private assets products. PG achieve the necessary liquidity and leniency on fees through adding transferable securities to the portfolio. The transferable assets include listed infrastructure, listed real estate, listed PE, opportunistic fixed income, traditional equity, debt, and hybrid instruments. (learn more of the only dedicated DC solutions funds run by dedicated private markets managers)

In March 2023, the FCA approved the first LTAF (Long-Term Asset Fund), which offers a diversified private markets portfolio with increased liquidity and regular redemption procedures.

LTAFs require both private markets and diversified long only capabilities and so are more suited to large traditional asset managers. Such examples include BlackRock, Aviva, and Schroders who have all launched respective LTAFs. BlackRock’s LTAF framework allocates assets as follows: 20-40% in real assets; 10-20% in private equity; 10-20% in private credit; 10-30% across multi-strategy credit; and further 10-30% in public equities to ensure liquidity and cost-effective management fees. One of the forementioned asset managers charges a 55bps flat fee, however, due to the lack of performance fee, DC pensions offer leniency and go above the 75bps cap.

Private market managers face challenges in creating LTAFs due to lacking internal long-only capabilities. This forces them to seek external avenues for exposure, incurring high charges and liquidity costs. The tight pricing restrictions make every basis point count, making large traditional firms with expertise in both public and private markets managers required. Nevertheless, this presents an opportunity for emerging GP’s. In the last year, firms have made the acquiring company’s liquid offerings, enabling them to generate greater liquidity for LTAF while remaining cost-competitive. Schroders’ £700m Evergreen to acquire GreenCoat Liquidity for LTAF to nearly transition through 2023 (another example is Oaktree’s acquisition of DDQ to access ETF and liquid products in 2021, who collaborated on a joint private credit offering (OCREDI) in the US, released late last year. This puts acquired businesses at an advantage when creating DC orientated products. There has been a significant increase in such acquisitions over the past two years including Arcmont (Nuveen), Alcentra (Franklin Templeton), AlbaCore (First Sentier) and Global Infrastructure Partners (Blackrock), to name a few. The trend is set to continue as traditional asset managers seek further diversification into the alternatives space through acquisitions.

Private Wealth: Growth of Private Wealth Investing in Alternative Strategies

UK wealth management AUM is increasing at 5.5% annually, currently sitting at £8.88 trillion (Statista, 2023), while private wealth investors are increasing their alternatives allocations by 12% annually (Bain & Co, 2023). These statistics demonstrate the need for GPs to prioritise private wealth fundraising.

However, private wealth investors face similar challenges to DC pensions regarding liquidity. While there are indeed similarities between the two, there are also notable differences. In contrast to DC investors, private wealth investors lack a charge cap and don’t adhere to a prevailing culture of “cost is king”. Consequently, they are willing to bear the fees commonly associated with private market strategies.

Furthermore, an additional issue that affects private wealth investors, but not DC schemes, is the minimum investment threshold. Many private equity firms require minimum ticket sizes ranging from £1m-$5m. From a sales team perspective, historically, it has not been deemed worthwhile for a team member to devote time to smaller ticket sizes, given the trade-off between time investment and prospective revenue generation.

Private Wealth: Creation of Private Wealth Evergreen Fund

GPs are actively creating specialised strategies for private wealth, often in the form of semi-liquid products, similar to those found in the DC market. In 2023, EQT, the Swedish alternative manager with €216 billion in assets, introduced EQT NEXUS. NEXUS offers a minimum ticket of €25,000, while offering monthly subscriptions, quarterly redemptions and providing exposure across all their notable funds. NEXUS attracted €100 million from both wealth and institutional investors within its first five months. (PEI, 2023) Similarly, Apollo venture into the space by launching the open-ended, semi-liquid Apollo Altermatives (AAA) fund in 2022. AAA requires a minimum ticket of $100,000 and targets 10-12% annual returns in lower volatility private markets. This fund received initial funding of $15 billion, with $10 billion coming from Apollo’s insurance affiliate Athene and an additional $5 billion from institutional investors (With Intelligence, 2023).

Apollo and EQT are just the tip of the iceberg with Hg Capital, Muzinich and Ares all recently releasing semi-liquid funds targeted to the wealth channels as well. Hg Capital announced a partnership with technology platform S64 in October 2023 to create an evergreen fund dedicated to wealth channels. In September 2023, Muzinich introduced an evergreen parallel lending strategy “Mloan European Evergreen Credit Strategy”, which features a 2% exit penalty in the first year. Ares, which has raised $4.5 billion in wealth channels over the past 12 months, also unveiled an open-ended vehicle in September 2023 known as “European Credit Solutions”. This offering is a UC Part 1 compliant version of their broader European Direct Lending strategy, which currently manages $55 billion in assets.

Moreover, private wealth orientated evergreen funds also attract additional institutional investments creating additional incentive and returns for managers. Partners Group’s Christian Wicklein, the Global Co-Head of Private Wealth, stated “if you look at our $43bn in evergreen AUM, around 40% of that is already from institutional investors” (Private Equity International, 2023). Institutional investor interest stems from notable differences with traditional closed ended private market funds, namely money being invested on day one, a very diversified product, and target allocations. While many successful funds have come to market for private wealth investors to access private markets, there remain a scarcity of such products and ample opportunities for new entrants. A survey conducted by Private Equity International in 2023, which included 101 GPs, revealed that only 21% of them had established dedicated strategies for private wealth channels (PE International, 2023).

Private Wealth: Establishing a Dedicated Private Wealth Sales Team

The creation of semi-liquid products has facilitated great success for the major players, but this has been alongside the expansion of their dedicated “private wealth solutions” sales teams covering private banks, wealth managers, family offices, and UHNWs.

Since GPs have historically concentrated their efforts on institutional investors, their existing sales teams do not have established connections and process expertise within the wealth channels.

Firms to undertake this expansion in Europe include Apollo, Ares, KKR, Ardian, Blackstone, Partners Group & Brookfield. Partners Group has a team of eight, up from two in 2021. KKR has a team of over ten, with nearly all joining from 2022 onwards. Blackstone boasts a team of ten, of nearly twenty individuals, and the vast majority joined within the last two years. To evidence the significance of building out such a network, have raised a total of $66bn from wealth channels, while Blackstone raised $48bn in 2022 alone (Preqin, 2022).

Alongside inhouse expansion, many GPs also leverage wealth platforms such as Moonfare and Titanbay. These platforms aggregate allocation from HNWIs and family office clients and so can accommodate much lower minimum ticket sizes of $100k, opening up the potential investor landscape to a much broader pool of smaller investors.

Institutional Opportunities: LGPS Pool

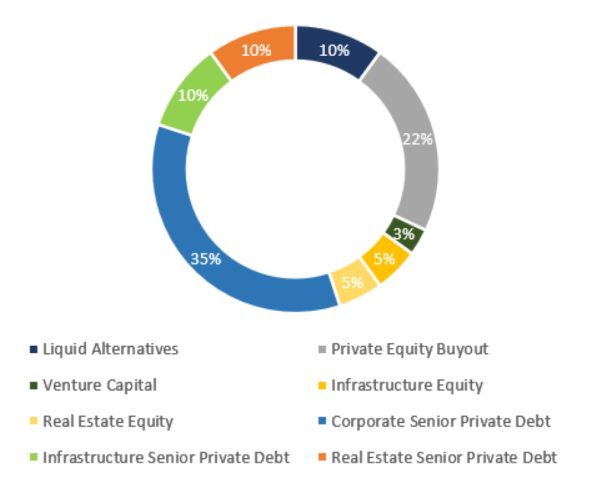

There are 86 local government pension funds in the UK, condensed into 8 individual pools based on region, managing £369 billion in AUM as of 2023 (LGPS Advisory Board, 2023). These pools are actively seeking opportunities to invest in illiquid asset strategies. LGPS were also part of the Mansion House reforms requiring them to increase their UK private markets allocations from 5% to 10%. Unlike their corporate DB counterparts, LGPS schemes are not going to furthur. Therefore, a lack of liquidity is not a concern for them. Consequently, many GPs have redirected their focus in the UK towards LGPS schemes. In 2022, LGPS pools significantly boosted their investments in illiquid assets, allocating a total of £10.1 billion, compared to the £8.4 billion allocated in 2021. A total of 87 alternative funds were awarded, with 20% directed towards Private Debt, 22% towards Private Equity, 35% towards infrastructure, 12% towards property, and 9% towards real assets and alternative investments (Pension Expert, 2022). A survey conducted by Alpha Real Capital in 2023 found professional, revealed that 91% of them anticipated increasing their exposure to illiquid alternatives in the future. Among them, 60% expected to raise their allocations by 5-10%, while 20% anticipated an even more substantial increase of over 10% in their illiquid asset allocations.

LGPS pools are very relationship orientated, a top-quality product isn’t traditionally enough to get them to invest, you must go to their conferences and nurture the relationship. Given that there is different levels of cooperation between the individual schemes in each respective pool, it is essential to have an individual spending the vast majority of their bandwidth covering LGPS. This is only multiplied by the fact that LGPS is the only UK pension pool looking to allocate substantial capital to illiquid assets.

Institutional Opportunities: Insurance

It was established earlier that insurers are buying out DB pension assets. The assets within UK insurance sat at $3.23 trillion in 2021, a $130bn increase from 2020 and growing $1.6 trillion since 2002 (Statista, 2023). Stepstone, the private markets dedicated investment firm, set up their own private markets portfolio for insurers.

With this continued growth and the diversified portfolios that insurance companies are looking to build, there are opportunities for private markets managers, across all strategies.

Private markets have historically represented under 10% of most insurance companies portfolios but a study by Ortec Finance indicates that insurance companies are committed to increasing their exposure to alternatives. 73% of London insurers stated that increased transparency and reporting around alternative investments has catalysed this.

Highlights from Ortec Finance’s 2024 insurance study include:

- 69% expect increases in exposure to private equity.

- 73% expect increases in exposure to private infrastructure.

- 70% expect increases in direct real estate investments.

- 63% expect increases in exposure to hedge funds.

The increase in UK insurance assets coupled with an increase in alternatives exposure has led to some firms hiring individuals to solely cover insurance. These firms include, Blackstone, ICG, and Apollo.

Institutional Opportunities: Investment Consultants

Another critical factor for alternative GP future capital raising efforts is maximising the effect of investment consultants. Consultants traditionally derived a significant portion of their revenue from DB schemes. With DB assets on the decline, consultants are actively seeking alternative investor types to sustain profitability in their advisory services. They have started to focus more on wealth managers, investor type they have historically worked with. An illustrative instance is the partnership between Mediolanum and St James’ Place (SJP), the British wealth manager with £153 billion in AUM. Redington is crafting tailored investment solutions for SJP’s clientele. Hence, as consultants diversify their investor base cultivating robust relationships with them opens avenues to access the capital pools in DC, LGPS, insurance and private wealth.

Consultants can also prove pivotal in the development of semi-liquid funds as they possess an intricate understanding of their clients’ needs and preferences. Collaborating closely with a consultant during the design process, therefore, essential. This collaboration approach ensures that all aspects, including product structure, fees, liquidity, redemption, and subscription options, are thoroughly considered. Resultingly, the crafted product will align with the expectations of the targeted investor base. To ensure the seamless and effective execution of this process, companies need a designated professional responsible for managing relationships with investment consultants. Leading firms such as KKR, Brookfield, OakTree, Tikehau, and Apollo all have a Consultant Relations specialist based in London to oversee the EMEA region. Even younger business with much smaller sales teams like T-Capital are making this strategic investment. These individuals have played a pivotal role in the development of the firms’ semi-liquid product offerings, the conventional rating process and the subsequent monetising of the rating.

Through widespread engagement with consultants, you can achieve a general increase in coverage across private wealth, DC, LGPS and insurance and the most effective way to ensure this broad general is having an individual with dedicated coverage. What is vital is that the person managing the consultant relations has all the right connections across the full spectrum of global, UK local and alternative specialist consultants.

Conclusion

The evolving landscape of institutional investing in the UK is reshaping the priorities and strategies of alternative investment managers. The traditional stronghold of DB pension schemes is diminishing, creating a pressing need for alternatives managers to explore new avenues for investor capital.

In this context GPs need to diversify their investor base, adapt their product offerings, and invest in new hires who can establish credible and long-term relationships.

GPs are having to shift their focus to other institutional LPs. Insurers are increasing their exposure to illiquid assets, while LGPS schemes continue to be a consistent source of capital. Many managers have now hired dedicated sales people for these segments.

Additionally, DC investors are becoming too significant of a capital pool to ignore and recent changes in regulation and further incentivising these growing schemes to invest in private markets. As it’s a segment that hasn’t been covered at all previously by GPs, there is a unique opportunity for early movers to invest in the right resources and take significant market share.

Similarly, coverage of wealth channels has become crucial for sustainable capital raising. Whilst previously only considered by the largest private markets managers, GPs of all sizes are starting to build in house teams and/or partnering with third party platforms.

Both wealth and DC channels require developing semi-liquid or evergreen funds tailored to their needs. Collaborating with investment consultants in creating these products is highly recommended for deeper insight into client needs and experienced consultant relations resources have also become in demand.

It’s important to emphasise that this presents a long-term strategy. It’s entirely feasible that a GP could raise more assets in the next couple of years by bringing on board a traditional institutional sales professional. Nevertheless, as we look ahead a few years and beyond, the increasing prevalence of evergreen funds and the growing portion of assets coming from private wealth and DC pensions suggest that the value of a private wealth sales team and a consultant relations team will continue to grow. To capture these future benefits, it’s crucial to lay the groundwork now, akin to the approach taken in private equity investments. Moreover, if you fail to this issue, your direct competitors are likely to do so and establish a track record, gaining a larger market share, which could present an insurmountable hill to climb.

European VC’s Shift Toward Dedicated IR

Capital Formation